The 15-Step Ultimate Mortgage Insider Package

Learn how to save thousands over the life of your Purchase or Refinance Loan

Specify Details on First Contact

When speaking with a mortgage lender or Broker for the first time, be very specific on your details. I.E. , your approximate credit score, plan down payment, whether you are W-2 income or self-employed. If the Home you’re purchasing is a single-family residence townhouse condo. If this is going to be a primary residence, second home or investment property.

Determine Your True Credit Score

Next is determining your proper credit score and This is very important as this will weigh heavily on your rate and or fees.. I recommend letting a lender or broker run your credit with what’s called a try merge credit report, which is what every lender in the United States will need ultimately anyway. The charges for these vary anywhere from $50-$100 per person. The reason why you want this report is because a lot of people like to use credit karma, their credit card score on their statement, basic service services like this that are not very accurate. You need a accurate credit report so whether or not you ultimately use this lender you need to know your true score.

Verify Your Qualifying Income

Next is determining your proper income that a lender can be used to qualify. If you were a W-2 borrower, your income is very easy to calculate. The lender will go off that W-2 and your current paystub. If your current paystub is making more money, they should be able to use the higher income. Where things get tricky, is if you are self-employed. That will typically require your last two years tax returns of self-employment. Lenders will typically ask for your last two years Business last two years Personal tax returns. They will then calculate your adjusted gross income after deductions.

Strive for a Conventional Loan

After the lender calculates your true income. Whether W-2 or self-employed, they should be trying to put you into a conventional loan. This will give you the best possible interest rate. If not, they may be trying to put you into an FHA loan, or if you’re self-employed into a bank statement loan. Brokers and Lenders get paid back from the lending institution they are selling too extra premiums; thus, some Lenders and Brokers push people into these Programs Even if they qualify for Conventional Financing.

Understanding Program Thresholds

Now the lender has enough information to figure out a rate points and closing cost for you. Meaning, they have figured your income out, figured your income, and have decided what type of program to put you in. Typically, this would be a conventional loan qualifying with a debt to income ratio of under 45% and a credit score typically of 620 or better. IMPORTANT. If your credit score in under 620 and or you have a high debt to income ratio, this is the time a Lender or Broker should recommend or place you into an FHA Loan.. If you are above 620 and your DTI is under 45% you should have conventional financing. Remember FHA financing has Funding Fees added to the Loan and carries mortgage Insurance. If you are self-employed and your score is above 620. The lender or broker will probably put you into some type of bank statement program using your last 12 months personal or business bank statements. These loans have a higher interest rate dependent on credit score and loan to value. Some statement programs go as high as 90%, but be aware the rate is significantly higher.

Leverage Negotiating Power Before Signing

Step six is now where it’s time to find out if you’re truly getting a good deal or not, and how to leverage your negotiating power, which you have a tremendous amount at this point in the game. After you sign your loan estimate aka LE your negotiating power diminishes a lot.. You as the consumer still have leverage and negotiating power if you already signed this ,but it makes for a harder conversation once Le is signed.

Request Quotes in Writing

Ask the broker or lender to send you a rate quote and terms , and approximate closing cost in writing.

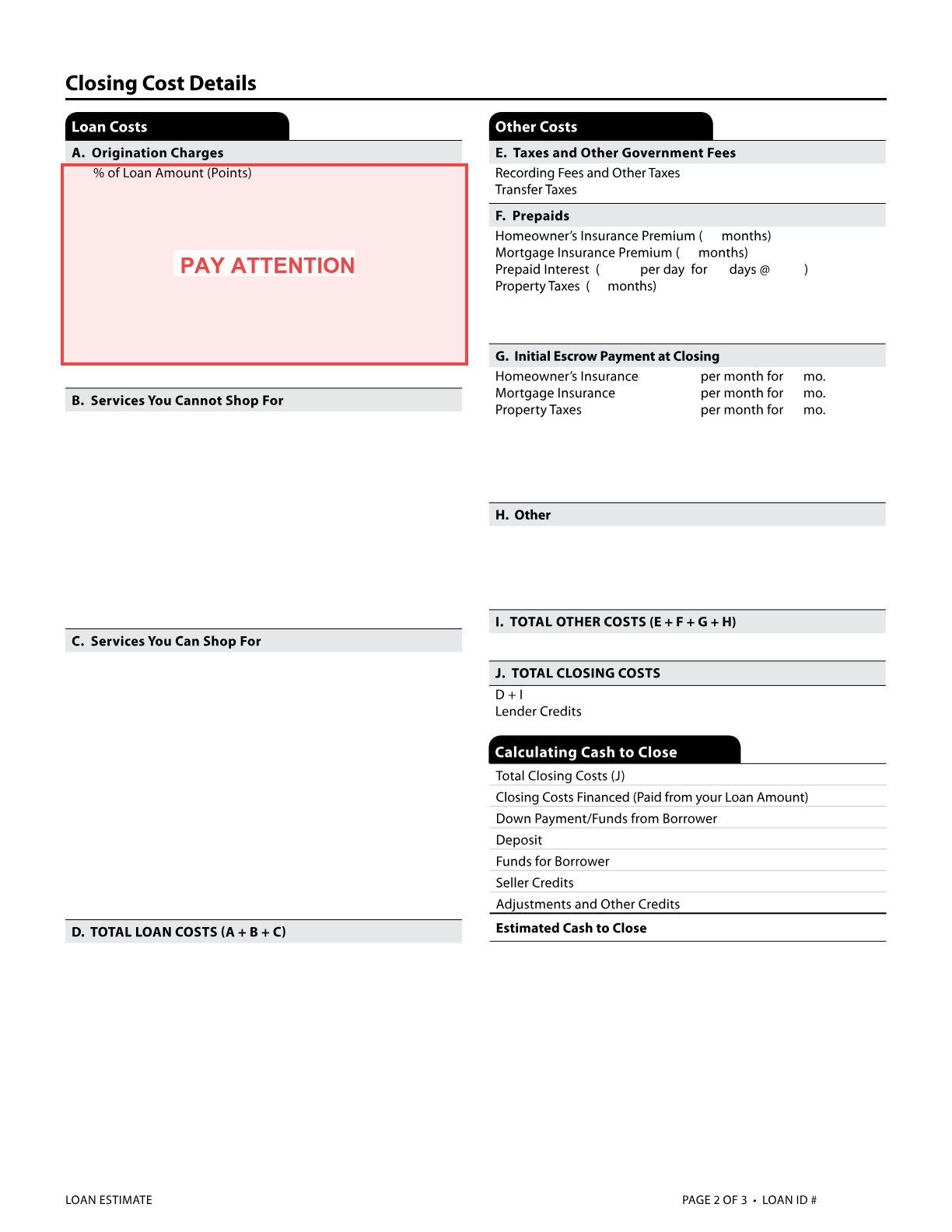

Verify Discount Points & Hidden Broker Fees

Example: Ask What is the current rate with my credit score and income for your particular program. The Broker or lender will probably quote you a rate. However you need to ask with my credit score and income are there any discount points (those are lender buy down rate points) origination, or Broker fees? ( those go to the mortgage broker and or lender). This part here is where people get hit hard with fees they aren’t even aware that they might not even have to pay. IMPORTANT. After you have shopped for the lowest rate, you should not be paying anymore then 1 point of your mortgage amount as a broker fee maximum. Also, any processing or underwriting fees you should tell lender you will not pay more than $995. total. This is a fair and standard fee for those items. Alot of Lenders and Brokers try for Thousands of dollars here BE AWARE... Studies have shown that borrowers pay between 1 to 3% of their loan amount in extra hidden or not properly disclose fees.

Demand Quotes Prior to the Loan Estimate (LE)

You might find that a lot of brokers and lenders like to do this verbally, they do this so there’s nothing in writing they can be held accountable for. I recommend highly that you push for it in writing.

Use Comparison Shopping Tools

Once you get there offer in writing, you are simply going to go to the link that I have at the top of our website where it says comparison shopping. This will take you to the popular bank rate website that is an incredible tool.. For free you simply put in all your details, i.e Credit, income, type of house, lots of specific questions so they can pinpoint the best lenders in the country with the best rates that day including the APR, which includes all fees. This is the tool that you will use to get quotes to see who the best in town is that day or week. Bank Rate is just one tool; there are many mortgage shopping sites I encourage you to use a few tools like this and shop around. Myself or my company has no affiliate agreement with Bank Rate or any other sites for compensation

Negotiate with Ammunition

Now that you have seen some quotes that typically will be much better than you probably were quoted by your mortgage broker or lender, you are now working with ammunition. Meaning you have the power to call or email your mortgage broker or lender, to let them know you have found much better deals in the open market. I would recommend when they ask you who it is with you do not disclose that information. Simply explain to that person that this is the rate points and APR that are available right now in my area. If you can match these terms, please put them in writing and I would be more than happy to continue our journey. However, if they cannot put this in writing, I recommend calling the lenders that are available that day or week with all your specifics from Bank Rate or whatever site, you find the best possible rate available. Please also keep in mind. I make no money or get any kickbacks or any financial gain by sending you to bank rate Or another mortgage rate shopping site or company. to shop for any loan. It is just a powerful tool, that you can use to negotiate with your current broker or lender if you choose to use them.

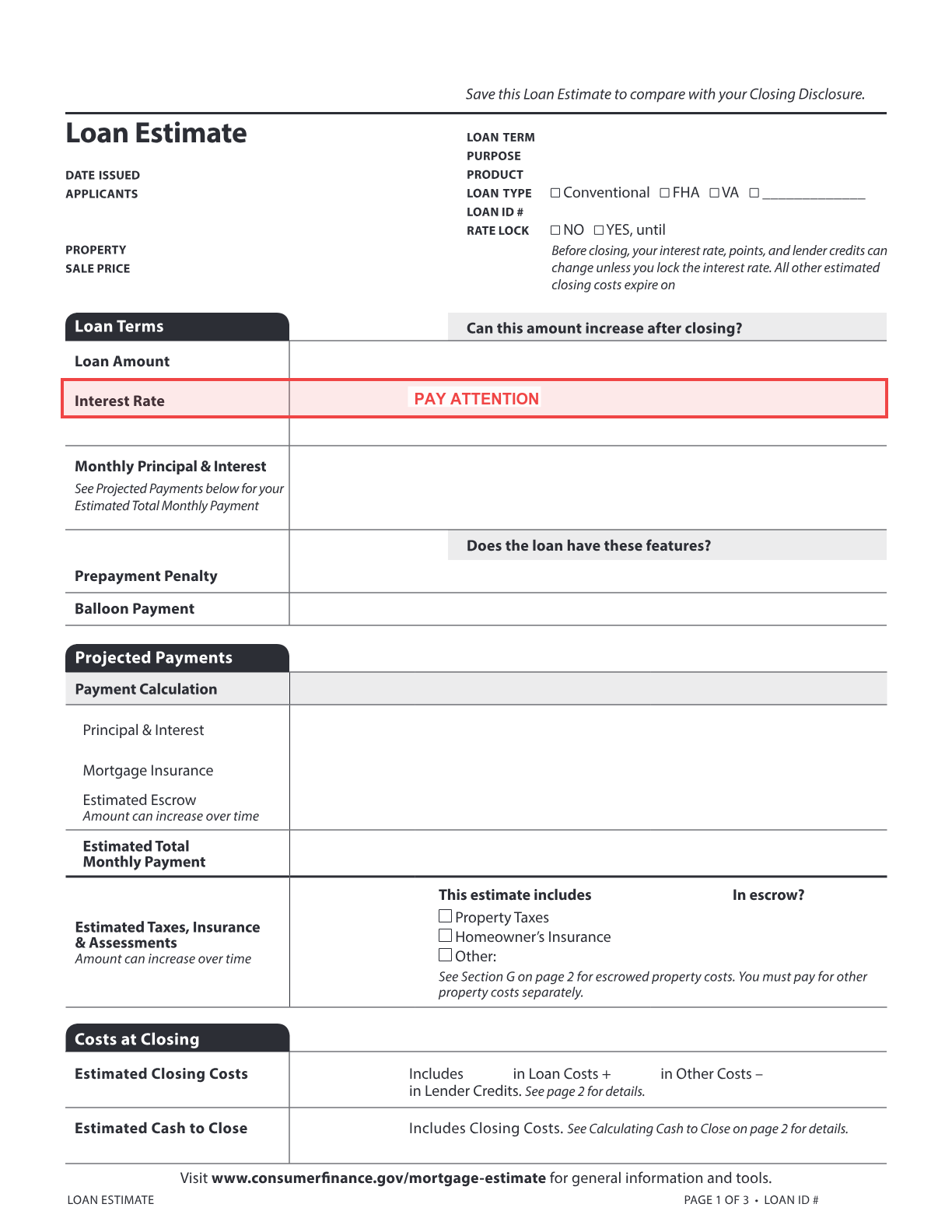

Audit the Loan Estimate (LE) Details

The LE or Loan estimate.

Lock in Your Rate Promptly

Let’s talk about rate locking. This is another important and tricky step, that requires knowledge and awareness. Often times your broker or lender may give you the option to lock in to the rate that was quoted to you, typically if you’re closing within 60 days, if you’re closing over 60 days, things can fluctuate more. But typically purchase and refinance loans or closed within 60 days.. So often times brokers and lenders will give you the option of locking in upfront or gambling, and seeing if things improve in the market. At the end of the day this Choice is ultimately up to you, however, I will tell you where it becomes sticky and you can run into problems. If you were happy with the rate quoted to you, I would recommend you tell your broker or lender to lock you in as soon as possible. This way you are guaranteed that rate. If you choose to gamble and see if interest rate rates improve, and the markets move against you. It could become very costly… some brokers and lenders will recommend that you wait to lock as they can sometimes capture more money that is paid back from the lender that they are selling the loan too.. it is in my opinion if you’re happy with the current rate that was quoted, lock it in immediately.

Query any Revised Loan Estimates

Congratulations as you have gotten through the hardest parts of the process and have in my opinion, fully done your due diligence and protected yourself in getting the best possible rate and fees. But still a few things just to protect yourself. At this point, typically an appraisal is ordered. And Loan Processor has typically reached out to continue your journey to get you to your closing with your disclosed loan estimate LE terms etc. The Processor will probably be looking for updated paystub’s, etc. stuff like that. If at any time during this process, your broker or lender tells you they’re sending you out a revised LE or loan estimate, you must ask them why? Sometimes for clerical or minor items this can be the case. However, if a mortgage broker or a lender change the terms on you, i.e. Your rate is different. Closing costs are different, you need to thoroughly compare it to the original that was signed and make sure nothing major was changed like rate, points, or fees. If something major was changed, I recommend not signing the document until you have thoroughly gone through it or showed it to another professional.

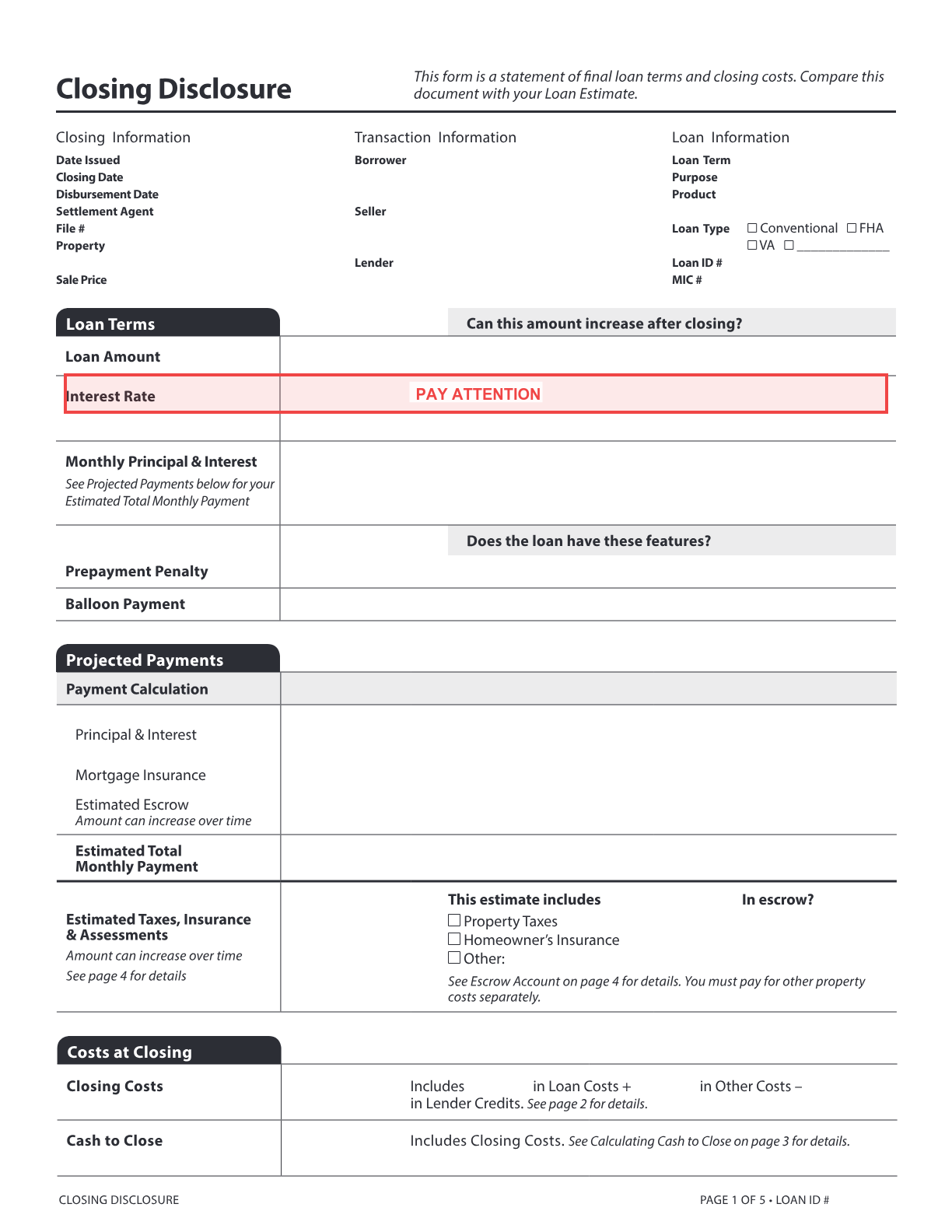

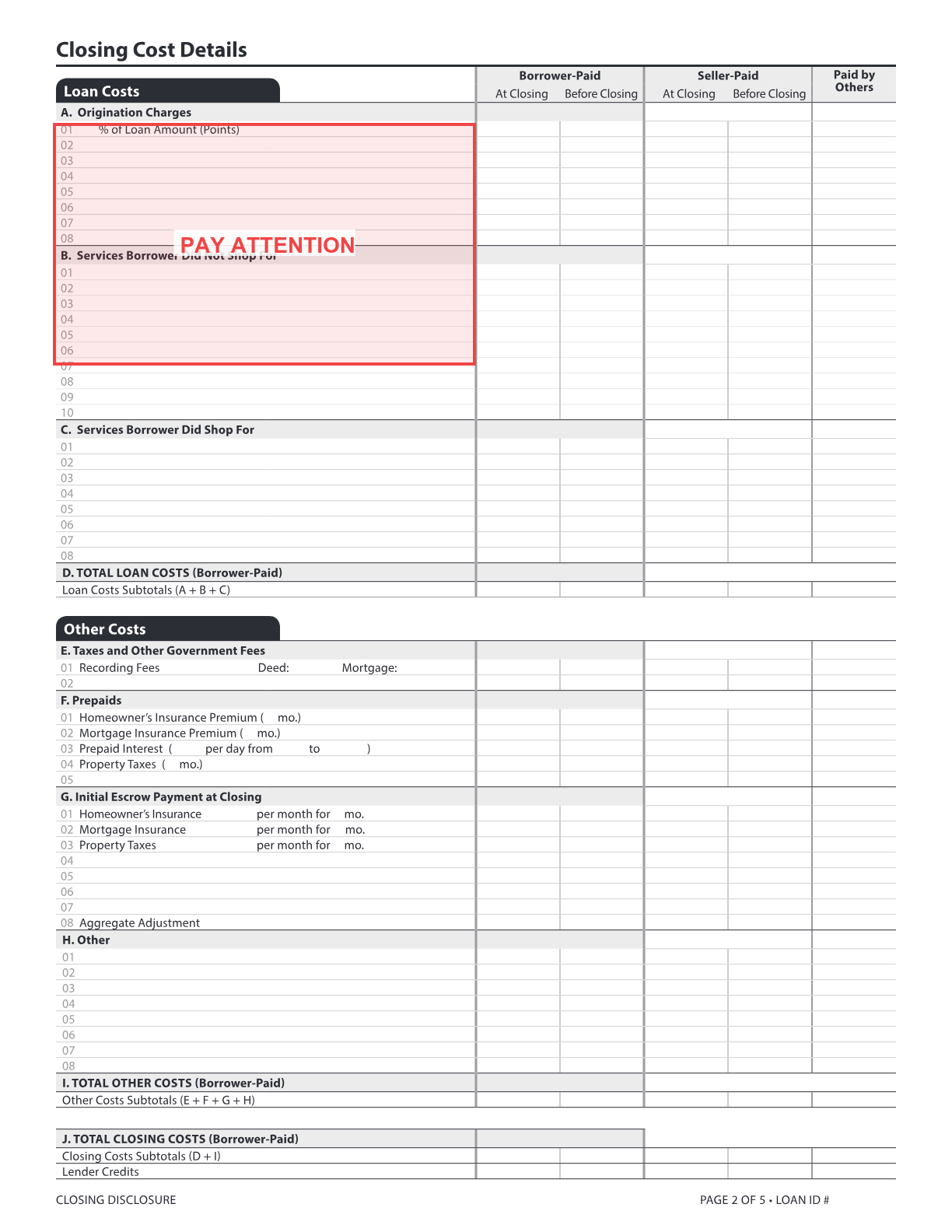

Compare Closing Disclosure (CD) to the LE & Post-Closing

CD or closing disclosure…

Post-closing: Congratulations on your closing.. Just a couple of last things to be aware of. First after you close make sure that the title company or closer send you a copy package of everything you signed. Down the road you may need these things for tax purposes, your survey, title, etc.. Also at closing Ask, the closer or Title company where your first payment goes. A lot of lenders sell their loans off right at closing. Meaning you can close with ABC Loans, and your first payment may be due to Bank Of America as an example. I have seen many times where clients borrowers not know where their first payment goes and end up with a 30 day mortgage Late because they didn’t know where their first payment goes so be specific to ask this. Sometimes this information is located in your closing package…

Closing Summary from Scott Leventhal

I hope you have found my ultimate mortgage insider package, helpful and useful..

Remember, saving just an 1/8 over of a percent on your rate can save you tens of thousands of dollars over 30 year mortgage as an example.. Let alone saving 1/4 -1/2 a percent.

Remember to shop and compare fees as well, you do not want to be overcharged with closing costs. Bank rate is one tool, however, going online using Claude or ChatGPT and asking who charges the least amount of points and best rate can be tremendously helpful in your negotiating power. And at the end of the day, this is what this is about.

Critical Warnings:

USING YOUR NEGOTIATING POWER BEFORE YOU SIGN A LOAN ESTIMATE OR LE…

ONCE YOU SIGN YOUR LE OR LOAN ESTIMATE AT A HIGHER RATE AND OR BEING OVERCHARGED FOR CLOSING COSTS IT IS LIKELY TOO LATE…

JUST FOLLOW MY STEPS TO SAVE MONEY, AND REMEMBER IF YOU NEED FURTHER PERSONAL CONSULTATION THAT SERVICES IS AVAILABLE THROUGH MY WEBSITE, I AM HAPPY TO HELP…

THANK YOU, AND I WISH YOU ALL THE BEST OF LUCK…

SCOTT LEVENTHAL

Weekly Insider Q&A Sessions

Join Scott Leventhal every Friday for a live, interactive Zoom meeting where he breaks down the mortgage steps one by one and answers your questions personally.

Add Weekly Friday Calls to Your Calendar

Secure your spot on your personal calendar so you never miss a live Q&A step-by-step breakdown.

Book Your 1-on-1 Consultation

Select an available date and time slot for your 1-hour Consultation with Scott.

Loading consultation calendar...